Abstract

This study aims to analyze the impact of fraud hexagon aspects (namely: stimulus, capability, collusion, opportunity, rationalization, and ego) on the fraudulent behavior intentions. A survey was conducted among 235 Budget User Officials from Regional Apparatus Organizations across 24 districts and cities in South Sulawesi province. Data collection used a questionnaire technique, where the number of questionnaires was distributed to 250 respondents/sample. The number of questionnaires collected and analyzed was 235. Data analysis was performed using Structural Equation Modeling - Partial Least Squares (SEM-PLS). The results indicate that the fraud hexagon aspects (namely ; stimulus, capability, collusion, opportunity, rationalization, and ego) postive significantly affect on the fraudulent behavior intentions. The study adds to the literature for the development of the Theory of Planned Behavior by investigating the fraud hexagon aspect in influencing behavioral intent, especially related to fraudulent behavioral intentions.

Keywords

Stimulus Capability Collusion Opportunity Ratinalization Ego Fraudulent Behavior Intentions

Introduction

Indonesia Corruption Watch (ICW) reports a continuous rise in corruption cases in Indonesia, with increases in the number of cases, suspects, and financial losses incurred by the state (ICW, 2023). Over the past three years, the trend has shown a significant escalation. In 2020, there were 444 cases involving 857 suspects, resulting in state losses of IDR 18.615 trillion. By 2021, cases rose to 533, with 1,173 suspects and losses amounting to IDR 29.438 trillion.

In 2022, the figures further increased to 579 cases, 1,396 suspects, and state losses of IDR 47.747 trillion. Case mapping based on perpetrator profiles indicates that State Civil Apparatus consistently represents the largest group of offenders, with 272 cases in 2020, 342 in 2021, and 223 in 2022. Given this trend, it is essential to analyze the factors driving State Civil Apparatus involvement in intention of fraud behavior (corruption).

The Theory of Planned Behavior (TPB) identifies three key determinants of behavioral intention: attitude toward behavior, subjective norms, and perceived behavioral control (Ajzen & Fishbein, 1972 ; Ajzen & Madden, 1986 ; Ajzen, 1991). These factors collectively shape behavioral intention, or an individual's readiness to act (Ajzen & Fishbein, 2010)(Ajzen & Fishbein, 2010). In this research, behavioral attitudes are conceptualized through stimulus, capability, and ego, while subjective norms are reflected in collusion and rationalization. Perceived behavioral control is represented by opportunity. Consequently, stimulus/pressure, capability, collusion, opportunity, rationalization, and ego serve as key determinants of fraudulent behavioral intentions. Empirical studies support this framework in the context of fraudulent behavior intentions. These six factors (namely ; stimulus/pressure, capability, collusion, opportunity, rationalization, and ego) as contributors to fraudulent behavioral intentions (Theotama et al., 2023). Opportunity, rationalization, and ego positively affect accounting fraudulent behavioral intentions, while stimulus/pressure, capability, and collusion do not (Siska et al., 2020).

Literature Review and Hypothesis Development

Theory of Planned Behavior

In this research, the Theory of Planned Behavior (TPB) is examined in relation to the role of behavioral intention in shaping behavior. TPB posits that individuals engage in a particular behavior when they have the behavioral intention to do so, and the stronger the behavioral intention, the greater the likelihood that the behavior will be carried out (Ajzen, 1985). Behavioral intention is determined by three key factors: behavioral attitude, subjective norms, and perceived behavioral control. The interaction of these factors leads to the formation of behavioral intention, or an individual's readiness to perform a behavior. The stronger an individual's attitude, perceived norms, and behavioral control, the stronger their behavioral intention to engage in the behavior (Ajzen & Fishbein, 2010).

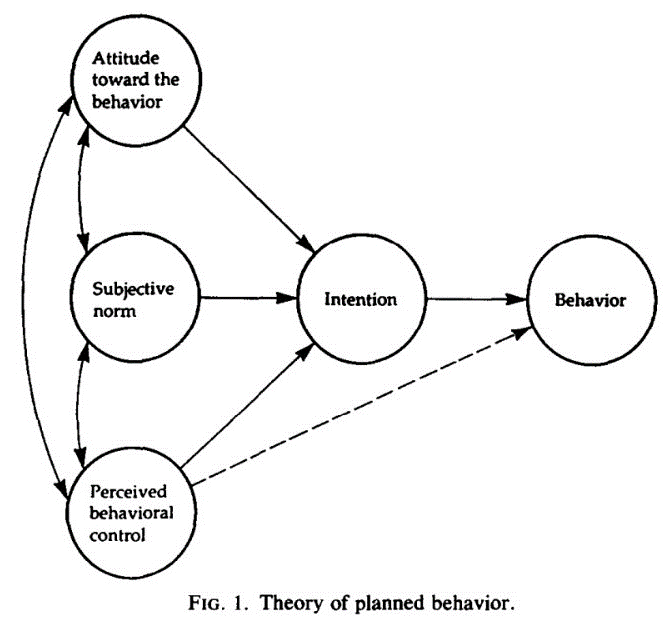

The constructs of behavioral attitude, subjective norms, and perceived behavioral control within TPB are examined in relation to the fraud hexagon framework. Behavioral attitude corresponds to the stimulus, capability, and ego aspects of the fraud hexagon. Subjective norms align with collusion and rationalization. While perceived behavioral control is associated with opportunity. Thus, the six elements of the fraud hexagon—stimulus, capability, collusion, opportunity, rationalization, and ego—contribute to an individual's behavioral intention to commit fraud. The stronger the behavioral intention to engage in fraudulent behavior, the greater the likelihood that the fraud will occur. A visual representation of the TPB model and its relationship to these factors is provided in the following figure.

Figure 1 Theory of Planned Behavior Model (Ajzen, 1991)

Fraud Hexagon Theory

The Fraud Hexagon Theory, also referred to as the SCCORE model, represents an acronym for six factors that contribute to an individual's or a group's propensity to engage in white-collar crime (Vousinas, 2019). White-collar crimes encompass various forms of financial misconduct, including corruption, financial crimes (Dearden, 2017), financial fraud (Dodge, 2020), and asset misappropriation (Billings et al., 2021). These six factors (stimulus/pressure, capability, collusion, opportunity, rationalization, and ego) as contributors to fraudulent behavioral intentions (Theotama et al., 2023). The fraud hexagon model is visually represented in the following figure.

Stimulus

Stimulus is pressure to commit fraud and has a financial and non-financial nature (Kazimean et al., 2019; Nair et al., 2023). Pressure to commit fraud can be divided into personal pressure, encouragement from the work environment such as co-worker encouragement or pressure from superiors, work pressure, external pressure, and each of these pressures is due to financial and non-financial factors (Kassem & Higson, 2012).

Capability

Cability as an ability, competence, capacity, skill, ethics, values, and , distinguishing characteristics, qualities, and attributes that individuals possess are deployed to carry out tasks (Odukoya & Samsudin, 2021). Capability is related to the ability of individuals who play an important role in committing fraud (Vousinas, 2019). There are many cases of fraud in large numbers without the right people and the right ability to do it (Wolfe & Hermanson, 2004).

Collusion

Asolution refers to an agreement to commit an act of fraud between two or more people, with one party bringing an action against the other for some criminal purpose, such as an act of fraud (Meidijati & Amin, 2022). If there is collusion, the risk of fraud is more significant, so the risk of collusion will affect the possibility of fraudulent acts (Achmad et al., 2022). Every criminal act cannot occur without the help of others (Ikechi & Anthony, 2020). Collusion plays an important role in determining the factors that lead to financial crime (Vousinas, 2019).

Opportunities

Individuals not only decide to commit fraud but choose when and where to do it. If there is a chance that they will get caught, they will avoid it (Ikechi & Anthony, 2020). A condition that can provide an opportunity to commit fraud; lack of supervision of the board of directors, weak control system to prevent/detect fraudsters, failure to discipline fraudsters, lack of access to information and lack of audit activities (Kassem & Higson, 2012 ; Omukaga, 2020).

Rationalization

Rationalization is a mindset that seeks justification before committing acts of fraud (Utomo et al., 2021). Rationalization is an important factor in the occurrence of fraudulent acts, because in the act of fraud, the perpetrator seeks justification for his behavior (Anan, 2021). Rationalization encourages a person to commit fraudulent acts because they are under stress so that the perpetrator feels that the action is natural or an ordinary act (Achmad et al., 2022).

Ego

Ego (arrogance) is a person's attitude of superiority combined with greed and the belief that internal supervision does not apply to him (Marks, 2014 ; Rahmatika et al., 2019). Ego attitude can be a factor in which a person will engage in fraudulent acts (Koomson et al., 2020).

Hypothesis Development

The Effect of Stimulus on Fraudulent Behavior Intentions

Stimulus in relation to the Theory of Planned Behavior (Ajzen, 1991) is a factor of subjective norms that causes the formation of behavioral intentions (Ajzen & Fishbein, 2010). Subjective norms have a positive and significant effect on behavioral intentions (Tianawati et al., 2023). In relation to stimulus perceived with subjective norms, individuals with high life pressure tend to show greater intention to commit fraud than individuals with low life pressure (Utami et al., 2019). Several research results show that stimulus affects the intention to commit fraud (Theotama et al., 2023). There is a linear relationship between the pressure/stimulus felt on the employee's intention to commit fraud (Mat et al., 2019). Thus, the following hypothesis can be formulated.

H1: Stimulus have a positive effect on fraudulent behavioral intentions.

The Effect of Capability on Fraudulent Behavior Intentions

Capability in relation to the Theory of Planned Behavior (Ajzen, 1991) is the control of behavior that leads to the formation of behavioral intentions (Ajzen & Fishbein, 2010). Perceived behavioral control has a positive and significant effect on behavioral intentions (Tianawati et al., 2023). In relation capabilities to perceived with behavioral control, individuals who have capabilities can encourage their intention to commit fraud. Research by Utami et al. (2019) and Djajadikerta & Susan (2020) prove that capability leads to intent to commit fraud. Capability effects the intention to commit fraud (Theotama et al., 2023). Thus, the following hypothesis can be formulated.

H2 : Capability has a positive effect on fraudulent behavioral intentions.

The Effect of Collusion on Fraudulent Behavior Intentions

Collusion in relation to the Theory of Planned Behavior (Ajzen, 1991) is a behavioral control that causes the formation of behavioral intentions (Ajzen & Fishbein, 2010). Perceived behavioral control has a positive and significant effect on behavioral intentions (Tianawati et al., 2023). Collusion is a sociological factor that affects an individual's intention to commit fraud (Maulidi, 2020). Collusion affects the intention to commit fraud (Theotama et al., 2023). Thus, the following hypothesis can be formulated.

H3: Collusion has a positive effect on fraudulent behavioral intention

The Effect of Opportunity on Fraudulent Behavior Intentions

Opportunity in relation to the Theory of Planned Behavior (Ajzen, 1991) is the control of behavior that causes to the formation of behavioral intentions (Ajzen & Fishbein, 2010). Perceived behavioral control has a positive and significant effect on behavioral intentions (Tianawati et al., 2023). In relation opportunity to the perceived with behavior control, the opportunity provided by the fraud perpetrator will have an impact on the intention to commit fraud. There is a linear relationship between perceived opportunities and employees' intentions to commit fraud (Mat et al., 2019). Opportunity has a positive effect on the intention to commit accounting fraud (Siska et al., 2020). Opportunity has a positive effect on the intention to commit fraud (Utomo et al., 2021). Opportunity affects the intention to commit fraud (Theotama et al., 2023). Thus, the following hypothesis can be formulated.

H4 : Opportunity has a positive effect on fraudulent behavioral intentions.

The Effect of Rationalization on Fraudulent Behavior Intentions

Rationalization in relation to the Theory of Planned Behavior (Ajzen, 1991) is a behavioral control that causes to the formation of behavioral intentions (Ajzen & Fishbein, 2010). Perceived behavioral control has a positive and significant effect on behavioral intentions (Tianawati et al., 2023). In relation to rationalization perceived by behavior control, rationalization can form behavioral intentions. Rationalization leads to the intention to commit fraud (Utami et al., 2019). Several research results show that rationalization has a positive effect on the intention to commit accounting fraud (Siska et al., 2020). Rationalization has a significant effect on the intention to commit fraud (Metts, 2021). Rationalization has a positive effect on the intention to commit fraud (Utomo et al., 2021). Rationalization affects the intention to commit fraud (Theotama et al., 2023). Thus, the following hypothesis can be formulated.

H5 : Rationalization has a positive effect on fraudulent behavioral intentions.

The Effect of Ego on Fraudulent Behavior Intentions

Ego or arrogance in relation to the Theory of Planned Behavior (Ajzen, 1991) is a behavioral attitude that causes to the formation of behavioral intentions (Ajzen & Fishbein, 2010). Several research results show that ego has a positive effect on the intention to commit fraud(Siska et al., 2020). Ego influences the intention to commit fraud (Theotama et al., 2023). Thus, a hypothesis can be formulated.

H6 : Ego has a positive effect on fraudulent behavioral intentions.

Research Design

Research Approach

This research employed a quantitative research approach using a survey method (Creswell, 2014;Neuman, 2014;Sekaran & Bougie, 2016) to analyze the causes of fraudulent behavior within local government. The survey targeted State Civil Apparatus, specifically budget user officials in Regional Apparatus Organizations (OPD) across 24 districts/cities in South Sulawesi province.

Sample selection and Variable Description

The sample size followed (Hair et al., 2019) which recommended a minimum of 5 to 20 times the number of variables analyzed. With eight variables in this research, the minimum required sample size was 140 respondents (7 × 20). A total of 250 questionnaires were distributed, and 235 valid responses were collected and analyzed. The research examined fraud hexagon factors—stimulus/pressure, capability, collusion, opportunity, rationalization, and egoas exogenous variables and with fraudulent behavior intentions as the endogenous variable. Variable measurements are presented in Table 1.

| No | Variable | Variable Measurement |

| 1 | Stimulus (ST) | a). Low income. b). High financial needs. c). Family pressure from lifestyle. d). Pressure from the work environment. e). Job pressure (Koomson et al., 2020 ; Dani et al., 2022) |

| 2 | Capability (CP) | a). Ability to excel over others. b). Ability to influence others. c). Position. d). Ability to master the situation. e). Ability to solve problems (Koomson et al., 2020 ; Dani et al., 2022) |

| 3 | Collusion (CL) | a). Group influence perspective. b). Social selection perspective. c). Instrumental perspective. d). Social change perspective (Vousinas, 2019) |

| 4 | Opportunity (OP) | a). Characteristics that are vulnerable to fraud. b). Ineffective management. c). Complex and unstable organizational structure. d). Inadequate internal control (Koomson et al., 2020 ; Dani et al., 2022) |

| 5 | Rationalization (RZ) | a). Just borrow and will return it. b). No party is harmed. c). For a good purpose. d). Deserve more ((Koomson et al., 2020 ; Dani et al., 2022) |

| 6 | Ego (EG) | a). Attitude is always better than others. b). Doesn't care about people's negative views of him. c). Not caring about decreasing/losing self-esteem. d). Not caring about the situation (Koomson et al., 2020 ; Dani et al., 2022) |

| 7 | Fraudulent Behavior Intentions (IB) | a). Intending. b). Trying. d). Trying again (Utomo et al., 2021) |

Source: Primary data that has been processed, 2024

Analysis Technique

This research aimed to analyze the role of behavioral intention in mediating the influence of fraud hexagon aspects (stimulus/pressure, capability, collusion, opportunity, rationalization, ego) on fraudulent behavior intentions using the Structural Equation Modeling - Partial Least Squares (SEM-PLS) analysis technique, based on the mediation model (Monecke & Leisch, 2012). The advantages of using SEM-PLS (Hair et al., 2017 ; (Hair et al., 2019) include: (a) the ability to test complex research models with many variables and indicators simultaneously, (b) its applicability to small sample sizes, and (c) its capability to measure both formative and reflective indicators.

Empirical Results and Analysis.

Respondents Characteristics Description

The majority of the questionnaires were distributed to government organizations, with 124 respondents (53%). In terms of education level, most respondents held a master's degree (S2), totaling 194 (82%), and regarding gender, the majority were male, accounting for 196 respondents (83%). The characteristics of the 235 respondents are presented in table 2.

| Descriptions | Criteria | Number | Percentage |

| Types of Organization | Secretariate Institution Inspectorate Department Office District | 10 36 11 124 7 47 | 4% 15% 5% 53% 3% 20% |

| Education Level | Undergraduate Graduate Postgraduate | 32 194 9 | 14 % 82 % 4 % |

| Sex | Male Female | 196 39 | 83 % 17 % |

Source: Primary data that has been processed, 2024

Validity Test

The validity test is determined by the magnitude of the loading factor for each construct, with values above 0.70 being highly recommended. The analysis results indicate that all indicators for each construct have loading factor values greater than 0.70, confirming their validity as measures of the respective constructs. The complete PLS Algorithm model and loading factors are presented in Table 3 below

| Statement Items | ST | CP | CL | OP | RZ | EG | BI |

| Loading Factor | |||||||

| 1 | 0.81 | 0.73 | 0.97 | 0.81 | 0.97 | 0.96 | 0.84 |

| 2 | 0.82 | 0.95 | 0.97 | 0.82 | 0.70 | 0.95 | 0.83 |

| 3 | 0.77 | 0.73 | 0.97 | 0.80 | 0.95 | 0.95 | 0.80 |

| 4 | 0.80 | 0.95 | 0.70 | 0.81 | 0.95 | 0.72 | - |

| 5 | 0.80 | 0.95 | - | - | - | - | - |

| Validity index | 0,70 | 0,70 | 0,70 | 0,70 | 0,70 | 0,70 | 0,70 |

| Remarks | Valid | Valid | Valid | Valid | Valid | Valid | Valid |

Source: Primary data that has been processed, 2024

Reliability test Test

The reliability test was assessed using Cronbach's alpha, with a threshold value greater than 0.70 indicating good reliability. The Cronbach's alpha values obtained for each construct are as follows: stimulus (0.86), capability (0.91), collusion (0.93), opportunity (0.83), rationalization (0.92), ego (0.92), and fraudulent behavior intentions (0.76). These results demonstrate that all constructs have Cronbach's alpha values greater than 0.70, indicating good internal consistency. The complete Cronbach's alpha values are presented in Table 4 below.

TABLE 4 : Reliability Test

| Variable | Cronbach’s alpha Coefficient | Cronbach’s alpha Index | Remarks |

| Stimulus (ST) | 0,86 | 0,70 | Reliable |

| Caapability (CP) | 0,91 | 0,70 | Reliable |

| Collusion (CL) | 0,93 | 0,70 | Reliable |

| Opportunity (OP) | 0,83 | 0,70 | Reliable |

| Rasionalization (RZ) | 0,92 | 0,70 | Reliable |

| Ego (EG) | 0,92 | 0,70 | Reliable |

| Fraudulent Behavior Intentions (IB) | 0,76 | 0,70 | Reliable |

Source: Primary data that has been processed, 2024

Evaluation of Structural Model

Structural model testing was conducted by examining the R² value, which serves as the Goodness of Fit test. The fraudulent behavior intentions construct yielded an adjusted R² value of 0.812, indicating that 81.2% of the variation in fraudulent behavior intentions is explained by the constructs of stimulus, capability, collusion, opportunity, rationalization, and ego (0.812 × 100%). The remaining 18.8% (100% - 81.2%) is explained by other variables not included in the research. The goodness of fit values are presented in Table 5 below

| Description | R Square | R Square Adjusted |

| Fraudulent Behavior Intentions | 0.817 | 0.812 |

Source: Primary data that has been processed, 2024

Hypothesis Test

The hypothesis test of the influence of the fraud hexagon aspects on the intention of fraudulent behavior can be seen from the coefficient value and p-value. The results of the analysis can be presented in table 6

| Variables | Original Sample (O) (Coefficient | Standard Deviation (STDEV) | t-Statistics (|O/STDEV|) | p- values | Hypothesis Test Results |

| Stimulus -> Fraudulent behavior intentions | 0.674 | 0.093 | 7.221 | 0.000 | H1 accepted |

| Capability -> Fraudulent behavior intentions | 0.111 | 0.152 | 3.729 | 0.002 | H2 accepted |

| Rationalization -> Fraudulent behavior intentions | 0.323 | 0.159 | 8.144 | 0.000 | H3 accepted |

| Collusion -> Fraudulent behavior intentions | 0.429 | 0.080 | 2.715 | 0.000 | H4 accepted |

| Ego -> Fraudulent behavior intentions | 0.272 | 0.042 | 3.918 | 0.006 | H5 accepted |

| Opportunity -> Fraudulent behavior intentions | 0.485 | 0.091 | 5.316 | 0.000 | H6 accepted |

Source: Primary data that has been processed, 2024

Discussion

The Effect of Stimulus on Fraudulent Behavioral Intentions

The results of the hypothesis test (H1) indicate that the coefficient value for the effect of stimulus/pressure on fraudulent behavioral intentions is 0.674, with a t-statistic of 7.221 and a p-value of 0.000. Since the t-statistic (7.221) exceeds the critical threshold of 1.96 and the p-value (0.000) is below 0.05, hypothesis 1 (H1) is accepted. These findings suggest that stimulus/pressure has a significant positive effect on fraudulent behavioral intentions, meaning that the greater the stimulus or pressure experienced by an individual, the stronger their behavioral intentions to commit fraud. This result aligns with the Theory of Planned Behavior, which identifies three key determinants of behavioral intention: attitude toward behavior, subjective norms, and perceived behavioral control (Ajzen, 1991). Stimulus/pressure is a component of attitude toward behavior that contributes to the formation of fraudulent behavioral intentions. Furthermore, these findings are consistent with prior research by Utomo et al.(2021) and (Theotama et al., 2023)Theotama et al.(2023), which also establish a positive relationship between stimulus/pressure and fraudulent behavioral intentions.

The Effect of Capability on Fraudulent Behavioral Intentions

The results of the hypothesis test (H2) indicate that the coefficient value for the effect of capability on fraudulent behavioral intentions is 0.111, with a t-statistic of 3.729 and a p-value of 0.002. Given that the t-statistic (3.729) exceeds 1.96 and the p-value (0.002) is below 0.05, hypothesis 2 (H2) is accepted. These results indicate that capability has a significant positive effect on fraudulent behavioral intentions, suggesting that individuals with a greater ability to commit fraud are more likely to develop an behavioral intention to engage in fraudulent activities. Thus, capability plays a role in shaping fraudulent behavioral intentions. This finding is consistent with the Theory of Planned Behavior, which identifies attitude toward behavior, subjective norms, and perceived behavioral control as the primary determinants of behavioral intention (Ajzen, 1991). Capability, as a factor influencing attitude toward behavior, contributes to the formation of fraudulent behavioral intentions. These results are also in line with previous studies by Utami et al. (2019) and Theotama et al.(2023), which highlight the role of capability in influencing fraudulent behavioral intentions.

The Effect of Collusion on Fraudulent Behavioral Intentions

The results of the hypothesis test (H3) indicate that the coefficient value for the effect of collusion on fraudulent behavioral intentions is 0.429, with a t-statistic of 2.715 and a p-value of 0.000. Since the t-statistic (2.715) exceeds the critical threshold of 1.96 and the p-value (0.000) is below 0.05, hypothesis 3 (H3) is accepted. These findings suggest that collusion has a significant positive effect on fraudulent behavioral intentions, meaning that as collusion increases, the behavioral intention to commit fraud also intensifies. This result aligns with the Theory of Planned Behavior, which identifies three key determinants of behavioral intention: attitude toward behavior, subjective norms, and perceived behavioral control (Ajzen, 1991).. In this context, collusion functions as a subjective norm that shapes behavioral intention. Furthermore, these findings are consistent with prior research by Theotama et al., (2023), which also establishes a positive relationship between collusion and the behavioral intention to commit fraud.

The Effect of Opportunity on Fraudulent Behavioral Intentions

The results of the hypothesis test (H4) indicate that that the coefficient value for the effect of opportunity on fraudulent behavioral intentions is 0.485, with a t-statistic of 5.316 and a p-value of 0.000. As the t-statistic (5.316) surpasses 1.96 and the p-value (0.000) is below 0.05, hypothesis 4 (H4) is accepted. These results indicate that opportunity has a significant positive effect on fraudulent behavioral intentions, implying that when opportunities to commit fraud arise, individuals are more likely to develop the behavioral intention to engage in fraudulent activities. This finding is consistent with the Theory of Planned Behavior, which posits that behavioral intention is influenced by attitude toward behavior, subjective norms, and perceived behavioral control (Ajzen, 1991). In this case, opportunity serves as a factor of perceived behavioral control that contributes to the formation of fraudulent intent. These results align with previous studies by Mat et al. (2019) and Theotama et al.(2023), which highlight the role of opportunity in shaping the behavioral intention to commit fraud.

The Effect of Rasionalization on Fraudulent Behavioral Intentions

The results of the hypothesis test (H5) indicate that that the coefficient value for the effect of rationalization on fraudulent behavioral intentions is 0.323, with a t-statistic of 8.144 and a p-value of 0.000. Since the t-statistic (8.144) exceeds the critical threshold of 1.96 and the p-value (0.000) is below 0.05, hypothesis 5 (H5) is accepted. These findings suggest that rationalization has a significant positive effect on fraudulent behavioral intentions, meaning that individuals who justify fraudulent actions are more likely to develop the behavioral intention to commit fraud. This result aligns with the Theory of Planned Behavior, which identifies three key determinants of behavioral intention: attitude toward behavior, subjective norms, and perceived behavioral control (Ajzen, 1991). In this context, rationalization functions as a subjective norm that shapes behavioral intention. Furthermore, these findings are consistent with prior research by Utami et al.(2019), Siska et al.(2020), Utomo et al.(2021), and Theotama et al. (2023), all of which establish a positive relationship between rationalization and the formation of fraudulent behavioral intentions.

The Effect of Ego on Fraudulent Behavioral Intentions

The results of the hypothesis test (H6) indicate that that the coefficient value for the effect of ego on fraudulent behavioral intentions is 0.272, with a t-statistic of 3.918 and a p-value of 0.006. As the t-statistic (3.918) surpasses 1.96 and the p-value (0.006) is below 0.05, hypothesis 6 (H6) is accepted. These results indicate that ego has a significant positive effect on fraudulent behavioral intentions, implying that individuals with strong ego-driven tendencies are more likely to develop the behavioral intention to engage in fraudulent behavior. This finding is consistent with the Theory of Planned Behavior, which posits that behavioral intention is influenced by attitude toward behavior, subjective norms, and perceived behavioral control Ajzen (1991). In this case, ego serves as a factor related to attitude toward behavior that contributes to the formation of fraudulent intention. The results support the ones obtained by Siska et al.(2020) and Theotama et al. (2023) which states that ego has a positive effect on fraudulent behavioral intentions.

Conclusion

This study aims to analyze the impact of fraud hexagon aspects (namely: stimulus, capability, collusion, opportunity, rationalization, and ego) on the fraudulent behavior intentions. The results indicate that the fraud hexagon aspects (namely ; stimulus, capability, collusion, opportunity, rationalization, and ego) postive significantly affect on the fraudulent behavior intentions.

Theoretical Contributions

This research contributes to the development of the Theory of Planned Behavior (TPB) which investigates the aspects of fraud hexagon (i.e., stimulus, capability, collusion, opportunity, rationalization and ego) as factors that form behavioral intentions. The fraud hexagon aspect is a development of the three aspects that form behavioral intentions from the Theory of Planned Behavior, namely behavioral attitude, subjective norms, and perceived behavioral control (Ajzen, 1991; Ajzen & Fishbein, 2010). Stimulus, capability and ego are the development of behavioral attitudes. Collusion and rationalization are the development of subjective norms. While, opportunity is the development of perceived behavioral control.

Managerial Contributions

Intention plays a role in determining a person's behavior, so the government needs to control factors that can encourage fraudulent behavior intentions, such as: First, implement a fair compensation system, reward performance, create a conducive work environment as an effort to reduce financial and non-financial pressure.Second, conducting ethics and anti-fraud training to improve anti-fraud competence. Third, commit not to give slippery money to avoid collusion. Fourth, strengthening the internal control system to reduce the opportunity of fraud. Fifth, encouraging more grateful behavior to control ego attitudes.

Limitations and Recomendation for future research

This study has several limitations :First, this study only examines and analyzes the direct influence of the hexagon fraud aspect on the intention of fraudulent behavior. Future research can develop an indirect influence research model to test and analyze the impact of the fraud hexagon aspect on fraud behavior by using behavioral intention as a mediating variable. In addition, it can explore moderation factors to test the fraud hexagon aspects of fraud behavior, such as individual morality variables. Second, this research only focuses on one public sector organization, namely government organizations, so it is necessary to develop research on other public sector organizations such as State/Regional Owned Enterprises, Political Parties, Educational Institutions, Community/ Religious Organizations.

References

- Achmad, T., Ghozali, I., & Pamungkas, I. D. (2022). Hexagon Fraud: Detection of Fraudulent Financial Reporting in State-Owned Enterprises Indonesia. Economies, 10(1), 1–16. DOI ↗ Google Scholar ↗

- Ajzen, I. (1985). From intentions to actions: a theory of planned behavior. Action Control, 11–39. DOI ↗ Google Scholar ↗

- Ajzen, I. (1991). The Theory of Planet Behavior. Organizational Behavior and Human Decision Processes, 50, 179–211. DOI ↗ Google Scholar ↗

- Ajzen, I., & Fishbein, M. (1972). Attitudes and Normative Beliefs As Factors Influencing Behavioral Intentions. Journal of Personality and Social Psychology, 21(1), 1–9. DOI ↗ Google Scholar ↗

- Ajzen, I., & Fishbein, M. (2010). Predicting Changing Behavior. In Taylor & Francis Group. DOI ↗ Google Scholar ↗

- Ajzen, I., & Madden, T. J. (1986). Prediction of Goal-Directed Behavior: Attitudes, Intentions, and Perceived Behavioral Control. Journal of Experimental Social Psychology, 22(5), 453–474. DOI ↗ Google Scholar ↗

- Anan, E. (2021). Determinants Fraudulent Financial Statements Using the S.C.O.R.E Model on Infrastructure Sector Companies in Indonesia. Ilomata International Journal of Tax and Accounting, 2(2), 113–121. DOI ↗ Google Scholar ↗

- Billings, A., Crumbley, L., & Knott, C. (2021). Tangible and Intangible Costs of White-Collar Crime. Journal of Forensic and Investigative Accounting, 13(2), 288–301. DOI ↗ Google Scholar ↗

- Creswell, J. W. (2014). Research Design : Qualitative, Quantitative, and Mixed Methods Approaches. SAGE Publications. DOI ↗ Google Scholar ↗

- Dani, R. M., Mansor, N., Awang, Z., & Afthanorhan, A. (2022). A Confirmatory Factor Analysis of the Fraud Pentagon Instruments for Measurement of Fraud in the Context of Asset Misappropriation in Malaysia. Journal of Social Economics Research, 9(2), 70–79. DOI ↗ Google Scholar ↗

- Dearden, T. E. (2017). An Assessment of Adults’ Views on White-Collar Crime. Journal of Financial Crime, 24(2), 309–321. DOI ↗ Google Scholar ↗

- Djajadikerta, H., & Susan, M. (2020). The Determinants of Students’ Intention to Conduct Fraud on Assignments and Examinations. Review of Integrative Business and Economics Research, 9(1), 119–124. http://buscompress.com/journal-home.html DOI ↗ Google Scholar ↗

- Dodge, M. (2020). A Black Box Warning: The Marginalization of White-Collar Crime Victimization. Journal of White Collar and Corporate Crime, 1(1), 24–33. DOI ↗ Google Scholar ↗

- Hair, J. F., Black, W. C., Babin, B. J., & Anderson, R. E. (2019). Multivariate Data Analysis (Eighth Edi). British Library Cataloguing. DOI ↗ Google Scholar ↗

- Hair, J. F., Hult, T. M., Ringle, C. M., & Sarstedt, M. (2017). A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM (Second Edi). SAGE Publications. DOI ↗ Google Scholar ↗

- ICW. (2023). Laporan Hasil Pemantauan Tren Penindakan Kasus Korupsi Tahun 2022 “Korupsi Lintas Trias Politika.” Indonesia Corruption Watch, 1–55. DOI ↗ Google Scholar ↗

- Ikechi, K. S., & Anthony, N. (2020). Fraud Theories and White Collar Crimes: Lessons for the Nigerian Banking Industry. International Journal of Management Science and Business Administration, 6(6), 25–40. DOI ↗ Google Scholar ↗

- Kassem, R., & Higson, A. (2012). The New Fraud Triangle Model. Journal of Emerging Trends in Economics and Management Sciences, Vol. 3(No. 3), 191–195. DOI ↗ Google Scholar ↗

- Kazimean, S., Said, J., Nia, E. H., & Vakilifard, H. (2019). Examining Fraud Risk Factors on Asset Misappropriation : Evidence from the. Journal of Financial Crime - Emerald Insight, 10(6), 24–62. DOI ↗ Google Scholar ↗

- Koomson, T. A. A., Owusu, G. M. Y., Bekoe, R. A., & Oquaye, M. (2020). Determinants of Asset Misappropriation at The Workplace: The Moderating Role of Perceived Strength of Internal Controls. Journal of Financial Crime, 27(4), 1191–1211. DOI ↗ Google Scholar ↗

- Marks, J. T. (2014). Playing Offense in a High-Risk Environment. Crowe Horwath,. Crowe Horwath, 94(8), 1–16. DOI ↗ Google Scholar ↗

- Mat, T. Z. T., Ismawi, D. S. T., & Ghani, E. K. (2019). Do Perceived Pressure and Perceived Opportunity Influence Employees’ Intention to Commit Fraud? International Journal of Financial Research, 10(3), 132–143. DOI ↗ Google Scholar ↗

- Meidijati, & Amin, M. N. (2022). Detecting Fraudulent Financial Reporting Through Hexagon Fraud Model: Moderating Role of Income Tax Rate. International Journal of Social and Management Studies (IJOSMAS), 3(2), 311–322. http://www.ijosmas.org DOI ↗ Google Scholar ↗

- Metts, S. (2021). The Relationship between Rationalization and Traits of Sympathy with One ’ s Intention to Commit. Southeastern Oklahoma State University United States. 12(12), 1–12. DOI ↗ Google Scholar ↗

- Monecke, A., & Leisch, F. (2012). Sempls: Structural Equation Modeling Using Partial Least Squares. Journal of Statistical Software, 48 (3). Journal of Statistical Software, 48(3), 1–32. DOI ↗ Google Scholar ↗

- Nair, S., Ramani, S., Tabianan, K., Perumal, I., & Jayabalan, N. (2023). Factors Affecting Accounting Fraud in Malaysian SMEs. Hong Kong Journal of Social Sciences, 60(No. 60 Autumn/Winter 2022). DOI ↗ Google Scholar ↗

- Neuman, W. L. (2014). Social research methods: Qualitative and quantitative approaches. International ed.) Boston: Peason Education. In Pearson. DOI ↗ Google Scholar ↗

- Odukoya, O. O., & Samsudin, R. S. (2021). Knowledge Capability and Fraud Risk Assessment in Nigeria Deposit Money Banks: The Mediating Effect of Problem Representation. Cogent Business and Management, 8(1). DOI ↗ Google Scholar ↗

- Omukaga, K. O. (2020). Is the Fraud Diamond Perspective Valid in Kenya? Journal of Financial Crime, 28(3), 810–840. DOI ↗ Google Scholar ↗

- Rahmatika, D. N., Kartikasari, M. D., Indriasih, D., Sari, I. A., & Mulia, A. (2019). Detection of Fraudulent Financial Statement; Can Perspective of Fraud Diamond Theory Be Applied to Property, Real Estate, and Building Construction Companies in Indonesia? European Journal of Business and Management Research, 4(6), 1–9. DOI ↗ Google Scholar ↗

- Sekaran, U., & Bougie, R. (2016). Research Methods for Business : A Skill-Building Approach. John Wiley & Sons, Inc. DOI ↗ Google Scholar ↗

- Siska, Zainai Basri, Y., Mariyanti, T., & Zulhelmy. (2020). S . C . C . O . R . E Model to Predict the Accounting Fraud Intension in Zakat Management Organization. International Journal of Business and Management Invention (IJBMI), 9(10), 28–36. DOI ↗ Google Scholar ↗

- Theotama, G., Waskita, Y. D., & Hapsari, A. N. S. (2023). Fraud Hexagon in The Motives to Commit Academic Fraud. Jurnal Ekonomi Dan Bisnis, 26(1), 195–220. DOI ↗ Google Scholar ↗

- Tianawati, A. K. A., Priantinah, D., & Malau, M. (2023). Application of the Theory of Planned Behavior and Fraud Triangle Theory in Preventing Academic Fraud Behavior among Indonesian Students. Journal of Behavioral Science, 18(1), 17–31. DOI ↗ Google Scholar ↗

- Utami, I., Wijono, S., Noviyanti, S., & Mohamed, N. (2019). Fraud Diamond, Machiavellianism and Fraud Intention. International Journal of Ethics and Systems, 35(4), 531–544. DOI ↗ Google Scholar ↗

- Utomo, B., Irianto, G., & Roekhuddin. (2021). The Effect of Individual Intention on Fraud Behavior. International Journal of Research in Business and Social Science (2147- 4478), 10(3), 369–379. DOI ↗ Google Scholar ↗

- Vousinas, G. L. (2019). Advancing Theory of Fraud: The S.C.O.R.E. Model. Journal of Financial Crime, 26(1), 372–381. DOI ↗ Google Scholar ↗

- Wolfe, D. T., & Hermanson, D. R. (2004). The Fraud Diamond: Considering the Four Elements of Fraud. DOI ↗ Google Scholar ↗